Why is Tether Buying Gold Like a Country?

How tokenised gold is emerging as a new store of value alongside USD stablecoins.

Tether’s rapid accumulation of physical gold has triggered a wave of commentary about what it means for the world’s largest stablecoin issuer. A recent Financial Times analysis (“Tether the Gold Whale”) observed that Tether is now buying gold at a pace comparable to mid-sized central banks, an extraordinary trajectory for a private company whose USD₮ stablecoin anchors global crypto liquidity.

Yet the real significance of this gold buying is not what headlines suggest. It is not a sign that USD₮ is becoming a gold-backed currency, nor that Tether is drifting away from the dollar. Instead, the gold accumulation reveals a far deeper strategic shift, one that could reshape how digital assets function as stores of value, how emerging markets access savings instruments, and how tokenised real-world assets begin to complement, rather than replace, the role of stablecoins.

To understand this shift, we need to separate what Tether’s gold buying does not mean from what it truly indicates about the future of digital money.

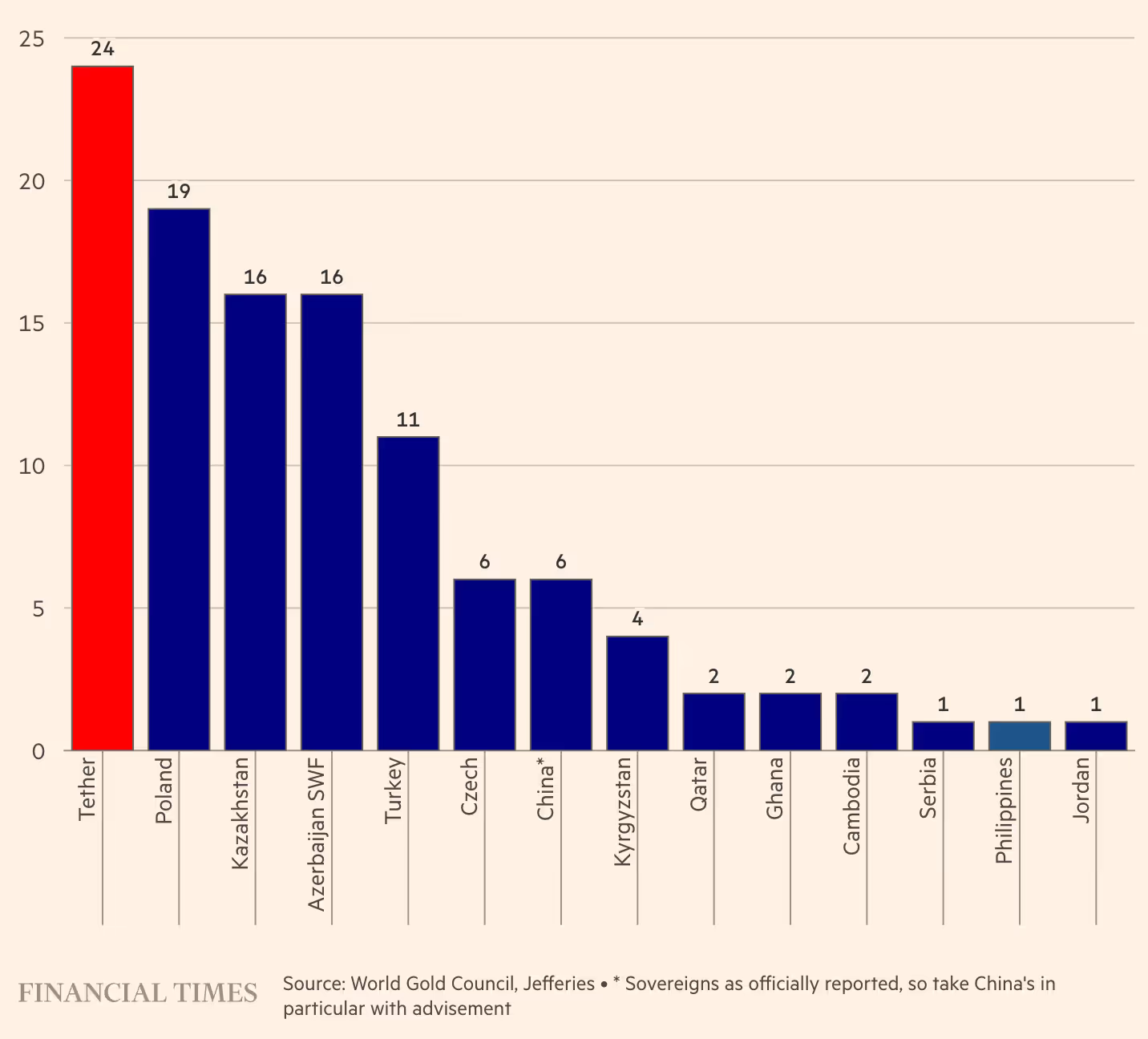

2025 net gold purchases, Tether vs select central banks

1. What Tether’s Gold Buying Does Not Mean

Despite speculation, gold has nothing to do with USD₮’s peg mechanism. Tether continues to back USD₮ overwhelmingly with short-term U.S. Treasuries, which provide the liquidity and price stability needed for a global settlement asset. Gold, by contrast, is too volatile and too slow to liquidate in a redemption cycle. This is why neither MiCA nor the U.S. GENIUS Act allows gold as a reserve asset for regulated payment stablecoins.

Tether’s gold reserves are not an attempt to alter USD₮’s backing model.

2. What the Gold Buying Actually Signals

The more interesting question is why Tether is buying gold at a scale normally associated with sovereign reserve managers. Here, the FT’s reporting provides a useful datapoint, the quantity, but the meaning lies elsewhere.

Part of the answer is macro-economic. Gold acts as a hedge against long-term fiat debasement, an idea that resonates strongly in emerging markets where inflation, currency controls, and banking fragility are real, everyday concerns. For many USD₮ users, particularly in Turkey, Argentina, Nigeria, and parts of the Middle East and Asia, holding gold is simply part of financial life. Tether’s own macro view appears to acknowledge this, and holding gold on its balance sheet reinforces its long-term resilience outside the U.S. banking system.

But the deeper strategic signal goes beyond macro hedging. Tether’s gold accumulation is also the foundation of an expanding digital-gold ecosystem centred around XAUt, its tokenised gold product. Tether is not buying gold because USD₮ needs it. It is buying gold because it is building a second monetary asset, a digital representation of physical bullion, designed for users who want a non-dollar store of value that still benefits from blockchain infrastructure. This is where gold intersects with Tether’s long-term product vision.

3. Tether’s Dual Monetary Architecture: Dollars for Settlement, Gold for Savings

Seen through this lens, Tether’s reserve strategy reveals a dual architecture.

On one side is USD₮, a dollar-denominated unit optimised for settlement, liquidity, and exchange integration. It behaves like the cash leg of the digital asset economy, fast, familiar, and liquid.

On the other side is XAUt, a digital representation of gold that functions much more like a savings asset. Gold’s role as a store of value is thousands of years old; tokenisation simply gives it the speed, divisibility, and accessibility that physical gold lacks.

Tether appears to be constructing a two-tier system: a fiat-based unit for transactions and a gold-based unit for wealth preservation. Far from competing with USD₮, tokenised gold complements it. Together, they start to resemble the architecture of a modernised, private-sector version of how fiat and gold once coexisted.

This is the strategic insight that goes beyond the FT’s reporting: Tether’s gold accumulation is a bet on the future of tokenised stores of value, not a departure from the dollar.

4. Who Might Use Tokenised Gold — and Why?

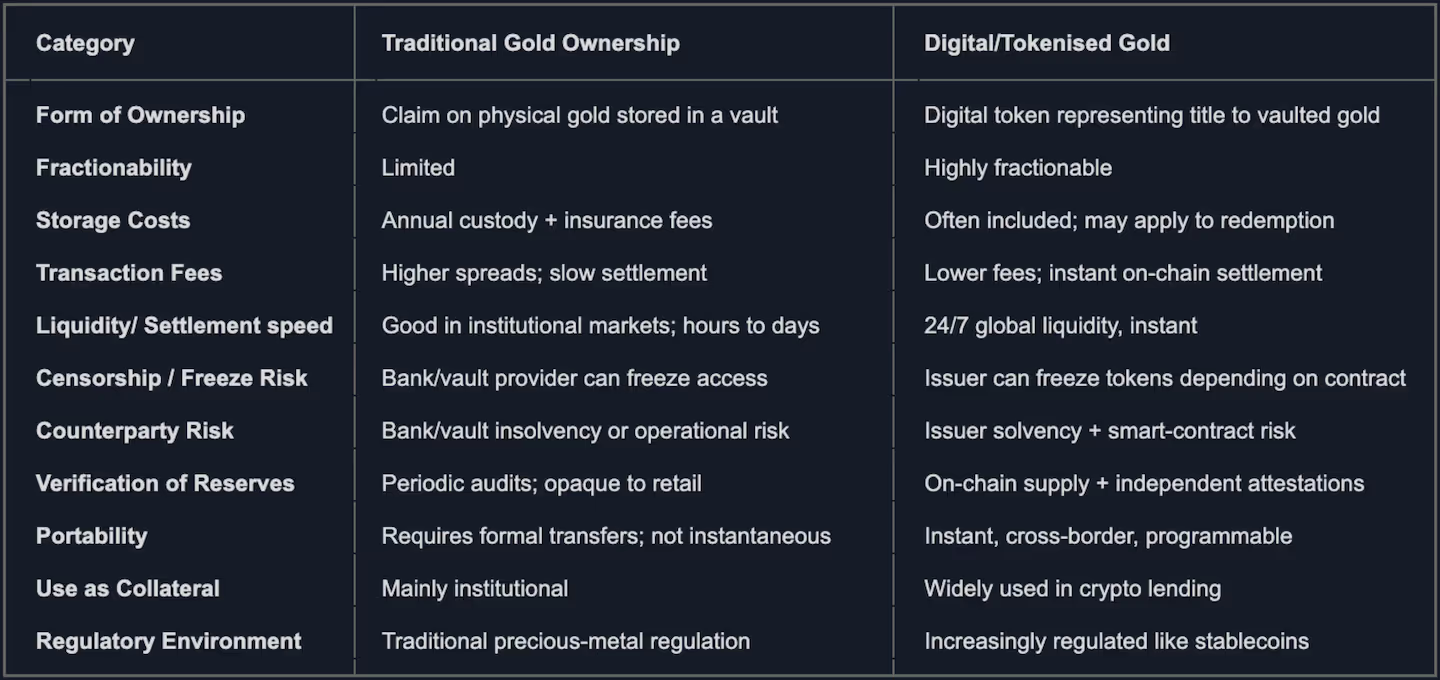

The potential user base for tokenised gold is much broader than often assumed. For individuals in high-inflation economies, gold is a natural hedge, but physical ownership is impractical, illiquid, and frequently restricted. Tokenised gold offers near-instant access, fractional ownership, and independence from local banks, without the costs associated with ETFs or vaulting services.

Comparison of traditional custodied gold and tokenised gold

Crypto users, too, are increasingly drawn to tokenised gold as an alternative to parking assets in USD-denominated stablecoins. During market stress, gold’s low correlation to crypto offers a different kind of refuge while still enabling fast on-chain transfers.

Institutions may find tokenised gold appealing as well, especially as collateral in lending protocols or structured products. Physical gold has deep global liquidity and is widely accepted as collateral in traditional markets; tokenising it brings that utility onto 24/7 settlement rails.

And finally, fintech platforms have a clear incentive to integrate tokenised gold as a simple savings product. Gold accumulation plans, common in parts of Asia and the Middle East, become easier to offer when they can be automated, fractionalised, and held securely on-chain.

Tokenised gold therefore bridges everyday savers, institutional finance, and crypto-native users, filling a role that neither USD-stablecoins nor physical bullion can serve on their own.

5. Why Did XAUt Scale While PAXG Remained Niche?

Before XAUt gained momentum, Paxos’ PAXG was the pioneering institutional-grade tokenised gold product. It remains well-regulated, carefully audited, and legally robust. Yet it never achieved the scale or distribution that XAUt now demonstrates.

Part of this difference is structural. Paxos operates under New York regulatory oversight, which brings safety but also friction. Issuance is slower, onboarding stricter, and product flexibility limited. XAUt, issued offshore by Tether, can expand more rapidly, mirroring the pace of Tether’s gold acquisitions.

Distribution also favoured XAUt. Tether’s ecosystem — built on years of network effects around USD₮ — offers deeper exchange integration, broader emerging-market reach, and more liquidity incentives. Users already familiar with USD₮ transition naturally into XAUt.

There is also a narrative dimension. For many users, especially in inflationary economies, XAUt feels like a digital evolution of something culturally familiar: gold savings. PAXG, by contrast, was designed primarily for institutional comfort, which limited its global retail adoption. Tether’s framing of gold as a macro hedge and a parallel store-of-value system resonates more strongly with its existing user base.

In short, PAXG was built for regulated institutions, while XAUt grew for the world that actually uses gold.

Comparison between PAXG and XAUt

6. What Tether’s Gold Strategy Means for the Future of Digital Money

Gold will not replace the dollar, and USD₮ will not morph into a gold-backed token. But tokenised gold is emerging as a complementary pillar of the digital asset economy. For the first time, individuals in high-inflation economies can hold and transfer gold with the same ease as a stablecoin. For the first time, gold can function as on-chain collateral without the inefficiencies of ETFs or futures. And for the first time, a private company is accumulating bullion at a scale comparable to sovereigns, not to support a currency peg, but to build a parallel store-of-value system powered by blockchain rails.

Tether’s gold strategy does not threaten USD₮. It strengthens the ecosystem around it. It acknowledges that the future of digital money will not be monolithic. It will combine fiat stability with asset-backed savings instruments, allowing users to choose between cash-like settlement and long-term wealth preservation, both tokenised, both accessible globally, and both operating outside traditional financial infrastructure.

In that sense, Tether’s gold reserves are not a departure from its stablecoin business. They are the beginning of a second, quieter transformation: the rise of tokenised gold as a global, digital savings asset.

Published on 07.12.2025

Adrien Bertholom

Others articles

Thought leadership

How large capital interacts with liquidity, inventory and execution in crypto markets.

Thought leadership

How programmable infrastructure reshapes digital asset treasury design and risk.