Beyond Structured Treasury: How On-Chain Financial Infrastructure Reshapes Foundation Risk

How programmable infrastructure reshapes digital asset treasury design and risk.

Digital asset treasury design is entering a new phase. The central question is no longer only how risk is distributed across payoff structures, but how the underlying financial infrastructure behaves.

In our previous article, Structured Product in Digital Assets : A Governance-first Overview for foundations, we examined structured treasury approaches in crypto foundations: how conditional payoff structures can redistribute risk when holdings are concentrated, volatile, and politically sensitive.

Those questions are not confined to foundations.

They increasingly apply to a broader class of digital asset treasury vehicles, including tokenized funds, corporate crypto reserves, staking ETPs, hybrid on-chain/off-chain structures, and emerging Digital Asset Treasury (DAT) issuers.

The shift underway is not simply about yield optimisation or volatility management. It is about infrastructure.

Structured products alter payoff profiles.

On-chain financial architecture alters behaviour.

For organisations issuing or managing digital asset treasury vehicles, understanding how infrastructure shapes behaviour is becoming central to fiduciary oversight.

From Instrument Design to Infrastructure Dependency

Traditional treasury products operate within layered institutional frameworks. Subscription, custody, valuation, clearing, and settlement are distributed across intermediaries operating under contractual and regulatory supervision. Risk is present, but it is framed through legal agreements and mediated by administrative processes.

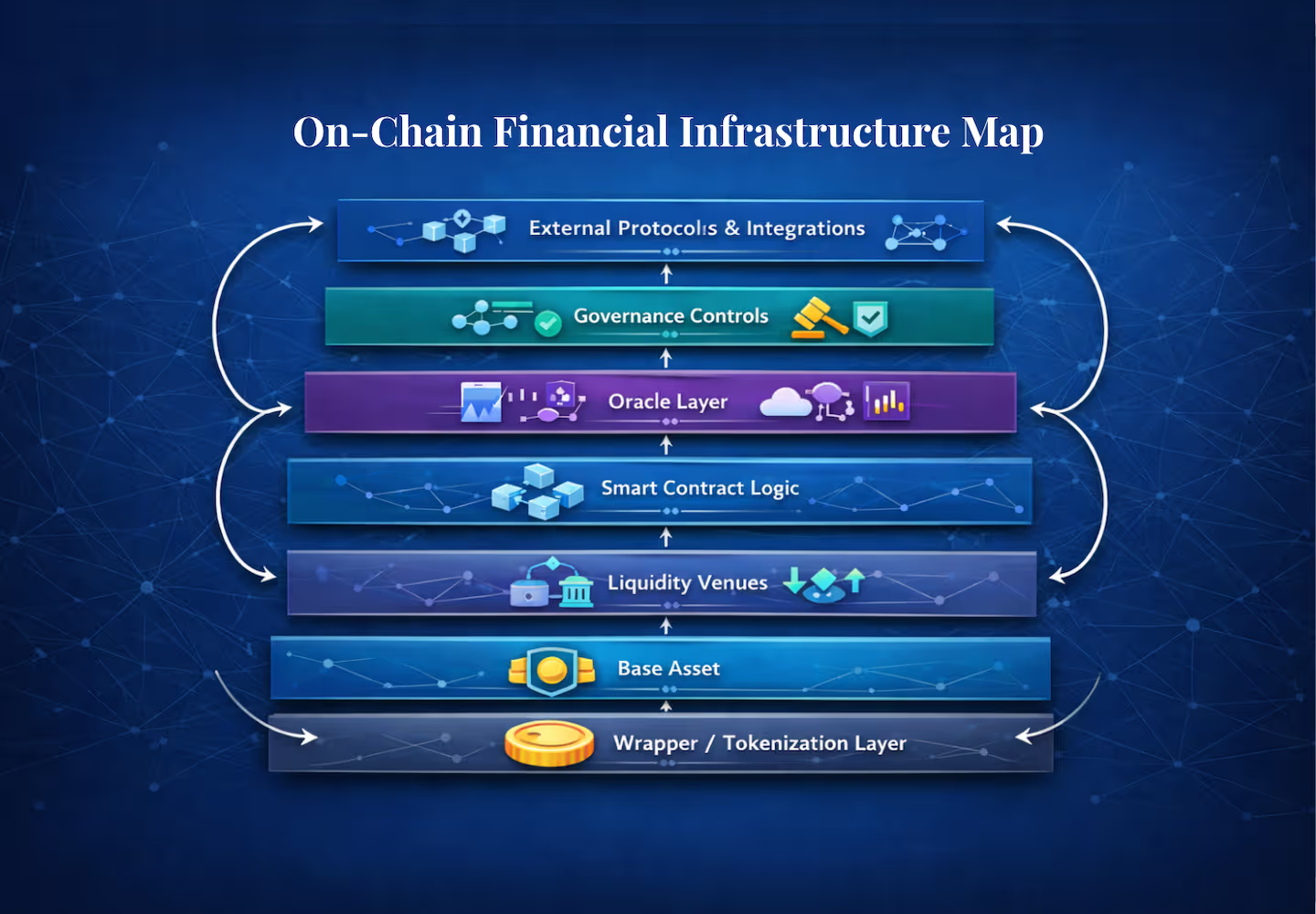

On-chain financial products reorganise these layers.

Minting and redemption can be encoded directly into smart contracts. Settlement becomes atomic rather than delayed. Reserve balances may be verifiable in real time, while transfer restrictions and investor eligibility can be enforced programmatically.

This architectural compression improves efficiency, but it also relocates risk.

Rather than relying primarily on institutional buffers, issuers must now depend on the integrity of the underlying infrastructure: code correctness, oracle reliability, liquidity depth, governance design, and the resilience of connected protocols. In programmable environments, infrastructure itself becomes part of the financial instrument.

For foundations, DAT issuers, and tokenized fund sponsors alike, this requires a broader analytical lens.

Structural Differences That Reshape Treasury Assumptions

Several structural characteristics distinguish programmable treasury systems from traditional financial vehicles.

Settlement Finality

Traditional products operate with reconciliation cycles and administrative reversibility. On-chain transactions, by contrast, settle instantly and irreversibly. Liquidity timelines compress dramatically, leaving little room for operational adjustment once transactions are executed. Treasury models must therefore account not only for price volatility but also for execution design and settlement mechanics.

Continuous Transparency

In many on-chain systems, balances and collateralization ratios are visible in real time. Transparency strengthens credibility but also removes informational buffers. During periods of volatility, stress indicators become observable simultaneously to all participants. Treasury ceases to be a periodic reporting exercise and instead becomes continuously visible infrastructure.

Composability

On-chain assets can, in principle, interact with other protocols. A transferable treasury token may be integrated into lending markets, paired in liquidity pools, or incorporated into structured yield strategies, provided it is supported by those platforms.

What matters is that once a treasury asset is programmable and transferable, the potential for inter-protocol interaction exists. That potential expands the structural risk surface, even when exercised selectively.

Governance Embedded in Architecture

Upgradeable contracts, multisignature controls, and token-based voting mechanisms embed governance directly within financial infrastructure. Protocol parameter changes may affect redemption conditions, liquidity incentives, or yield distribution. In programmable systems, financial architecture and governance architecture increasingly converge.

The comparison illustrates how risk migrates as financial infrastructure becomes programmable. Institutional buffers are replaced by systems governed by code, liquidity, and protocol design. Resilience increasingly depends on the strength of that infrastructure.

The Expanded Risk Surface

Building on the earlier discussion of structured treasury overlays, programmable infrastructure introduces additional dimensions of exposure.

Smart contract design replaces elements of contractual enforceability. Oracle dependencies influence valuation integrity. Liquidity assumptions may diverge significantly between stable conditions and periods of market stress. Where composability exists, cross-protocol dependencies can transmit shocks rapidly across interconnected layers.

These features do not inherently weaken digital asset treasury vehicles. They change how those vehicles behave.

The relevant question for boards and treasury committees is therefore not whether risk exists, but where it resides and how it may propagate.

Understanding redemption pathways under stress, liquidity fragmentation dynamics, oracle architecture, and governance controls becomes as important as modelling volatility bands or yield expectations.

Strategic Opportunities in Programmable Treasury Design

The expansion of infrastructure risk is matched by an expansion of design capability.

Programmable treasury systems enable automated rebalancing, conditional capital deployment, transparent proof-of-reserves, dynamic yield allocation, and real-time reporting. These features allow treasury operations to move beyond static balance sheet management.

More significantly, treasury instruments themselves can become infrastructure within broader ecosystems. Tokenized reserves may anchor liquidity, serve as collateral primitives, or support internal economic mechanisms.

In such environments, treasury ceases to be passive inventory. It becomes an operational layer within the financial architecture of a network.

Issuers that approach programmable infrastructure with discipline can convert transparency and automation into structural advantages.

Implications for Issuers and Oversight Bodies

For crypto foundations, this shift implies that treasury design must extend beyond structured overlays toward full infrastructure mapping.

For DAT issuers and tokenized fund sponsors, product design increasingly requires system-level risk analysis rather than instrument-level modelling alone.

For corporate crypto treasuries, it means recognising that liquidity and redemption behaviour may depend not only on market prices but also on protocol conditions.

Across these categories, oversight bodies should be able to articulate the full minting and redemption lifecycle, the behaviour of liquidity under stress, oracle and pricing dependencies, governance authority over contract upgrades, and the location of cross-protocol exposures.

These are infrastructure questions rather than purely financial ones.

Conclusion

The evolution from structured treasury overlays to programmable financial architecture marks a structural inflection point in digital asset markets.

Treasury vehicles are no longer defined solely by their payoff structures. They are defined by the systems within which those payoffs are generated, transmitted, and settled.

On-chain infrastructure compresses settlement, increases transparency, enables composability, and embeds governance within financial mechanics. As a result, treasury management increasingly resembles infrastructure design.

For foundations, DAT issuers, tokenized funds, and corporate crypto treasuries alike, the discipline required extends beyond financial modelling toward infrastructure literacy.

The next stage of digital asset treasury management will be determined less by yield optimisation and more by how effectively infrastructure risk is mapped, governed, and communicated.

𝘛𝘩𝘪𝘴 𝘮𝘦𝘴𝘴𝘢𝘨𝘦 𝘪𝘴 𝘧𝘰𝘳 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯𝘢𝘭 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺 𝘢𝘯𝘥 𝘥𝘰𝘦𝘴 𝘯𝘰𝘵 𝘤𝘰𝘯𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵 𝘢𝘥𝘷𝘪𝘤𝘦. 𝘐𝘭𝘭𝘶𝘴𝘵𝘳𝘢𝘵𝘪𝘰𝘯 𝘨𝘦𝘯𝘦𝘳𝘢𝘵𝘦𝘥 𝘸𝘪𝘵𝘩 𝘊𝘩𝘢𝘵𝘎𝘗𝘛.

Published on 04.03.2026

Taym Moustapha

Others articles

Thought leadership

Why bear markets expose fragile liquidity and broken market structure in crypto.

Thought leadership

A governance-first overview of structured products in digital asset markets for foundations.